Market Focus for the Week Ending on June 13th 2025

Market Focus for the Week Ending on June 13th 2025

Stocks Down Over Middle East Tensions:

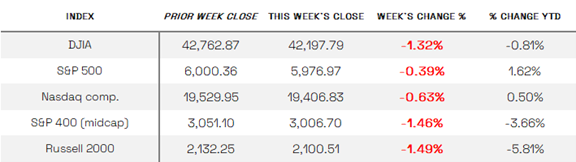

U.S. stocks reversed early gains and declined for the week amid escalating tensions in the Middle East. While markets were broadly higher through Thursday—bolstered by better-than-expected economic data and progress in U.S.-China trade talks, including the possibility of an extended tariff pause—sentiment soured on Friday following reports that Israel had launched airstrikes on Iranian nuclear facilities and military leaders, prompting a retaliatory response from Iran. This sharp escalation drove oil prices higher, lifting energy stocks but weighing heavily on broader indexes. The Dow Jones Industrial Average fell 1.32%, slipping back into negative territory for the year, while the S&P MidCap 400 and Russell 2000 dropped 1.46% and 1.49%, respectively; the S&P 500 and Nasdaq Composite declined more modestly but remained positive year-to-date.

DOW & TECH

THE DOW JONES INDUSTRIAL AVERAGE (DJIA) is the oldest continuing U.S. market index with over 100 years of history and is made up of 30 highly reputable “blue-chip” U.S. stocks (e.g. Coca-Cola Co., Microsoft).

The Dow ended the week down 1.32% at 42,197.79.

THE NASDAQ COMPOSITE INDEX tracks most of the stocks listed on the Nasdaq Stock Market – the second-largest stock exchange in the world. Over half of all stocks on the NASDAQ are tech stocks.

The tech-driven Nasdaq ended the week down 0.63%, closing at 19,406.83.

LARGE, MEDIUM, & SMALL CAP

THE S&P 500 LARGE-CAP INDEX is a market-capitalization-weighted index of 500 leading publicly traded companies in the U.S. The S&P 500 is regarded as one of the best gauges of prominent American equities’ performance, and by extension, that of the stock market overall.

The S&P 500 ended the week down 0.39%, closing at 5,976.97.

THE S&P 400 MID-CAP INDEX is the benchmark index made up of 400 stocks that broadly represent companies with midrange market capitalization between $3.6 billion and $13.1 billion. It is used by investors as a gauge for market performance and directional trends in U.S. stocks.

The S&P 400 mid-cap ended the week down 1.46%.

THE RUSSELL 2000 (RUT) SMALL-CAP INDEX measures the performance of the 2,000 smaller companies included in the Russell 3000 Index. The Russell 2000 is managed by London’s FTSE Russell Group and is widely regarded as a leading indicator of the U.S. economy because of its focus on smaller companies that focus on the U.S. market.

The Russell 2000 ended the week down 1.49%.

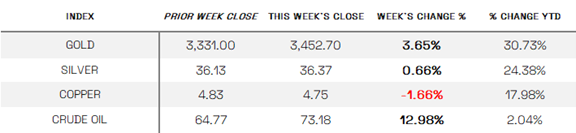

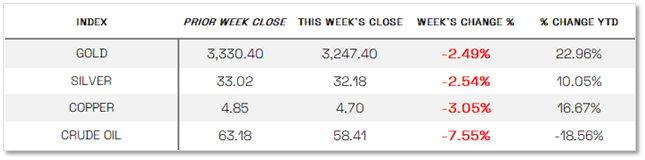

U.S. COMMODITIES / FUTURES OVERVIEW

THIS WEEK’S ECONOMIC NEWS

Labor Market Cooling Signs:

New jobless claims jumped to 242,000 last week, the highest in nearly 10 months, while the four-week average rose to 227,000. This suggests a gradual softening of the labor market. The University of Michigan’s preliminary consumer sentiment index also dropped to 65.6 — a seven-month low — on concerns about inflation and interest rates. Investors are now more closely watching for signs that could influence Fed policy decisions at the June meeting.

Earnings Focus:

The 1st Quarter 2025 earnings reporting season is nearly complete, with 99% or 497 companies having reported results. Of these, 76% have reported earnings above analyst expectations — in line with the 5- and 10-year averages of 77% and 75%. The blended year-over-year earnings growth rate for the S&P 500 stands at 13.7%, while revenue growth is tracking at 5.0%.

At the sector level, 8 of the 11 sectors have reported positive earnings growth, led by Communication Services and Health Care. Energy posted the largest decline relative to Q1 2024. The forward four-quarter P/E ratio for the S&P 500 is now 22.4, which remains above the 10- and 30-year historical averages.

Looking ahead, just 1 S&P 500 company is scheduled to report Q1 results next week, and 5 companies are expected to report for Q2.

THIS WEEK’S HIGHLIGHTED STORY

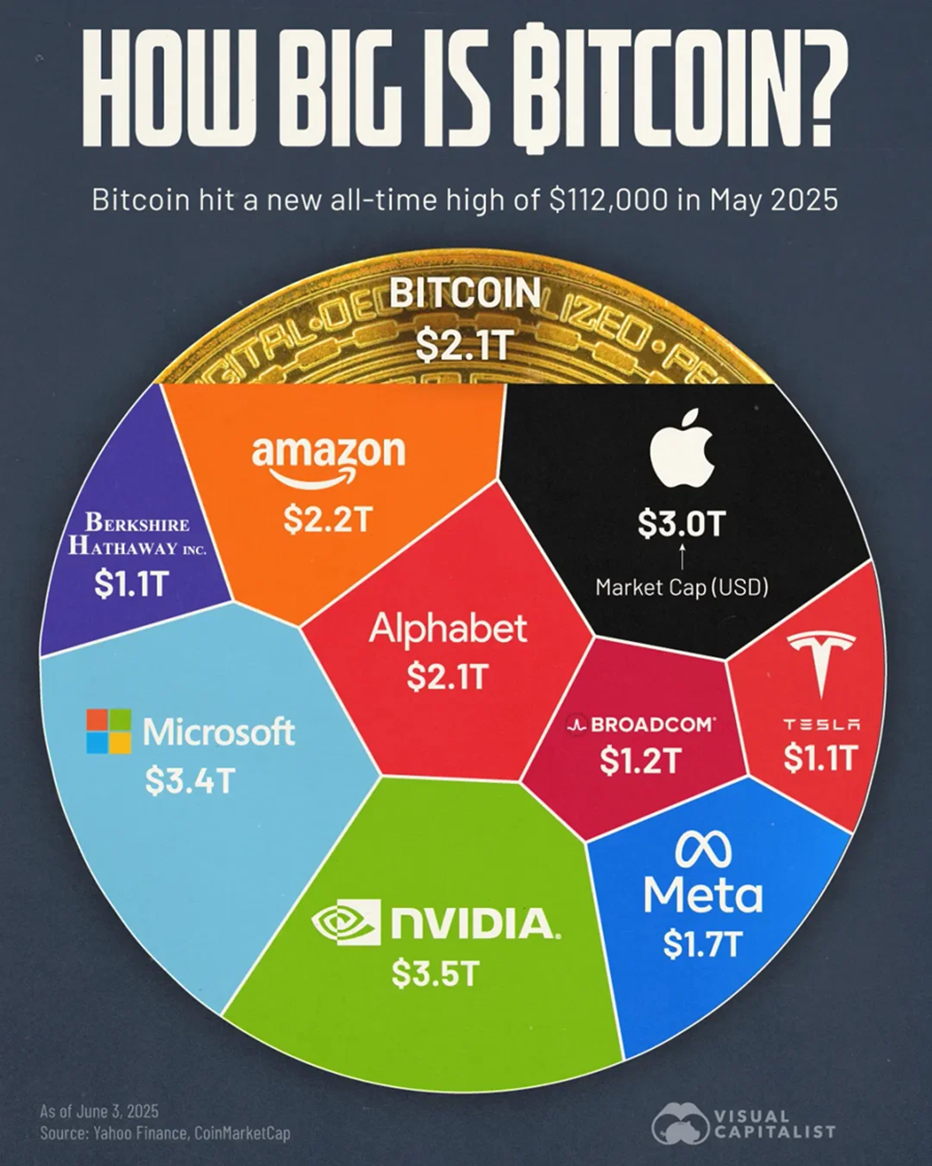

https://www.visualcapitalist.com/how-big-is-bitcoin-compared-to-the-worlds-largest-companies/

June 13, 2025

What We’re Showing:

Bitcoin reached its all-time high of $111,814 in May, marking a significant milestone in its price history. The infographic above compares Bitcoin’s valuation to the largest publicly-traded companies, highlighting its new position among global titans. The cryptocurrency now sits comfortably in the top five assets by market cap. The data for this visualization comes from CoinMarketCap and Yahoo Finance. It ranks the largest companies and bitcoin by market capitalization as of June 2025.

Key Takeaways:

Bitcoin has overtaken big names like Meta and Tesla and is now valued at $2.1 trillion compared, similar to Alphabet’s valuation. The rise follows renewed interest from institutions and political momentum behind crypto legislation. President Trump’s backing of a stablecoin bill has been a notable tailwind for digital assets in 2025.

Tech firms account for eight of the ten largest assets globally, including Microsoft, Apple, Amazon, and Meta. Even Tesla and Broadcom, though smaller, maintain trillion-dollar valuations.

Nvidia is the most valuable company in the world, with a $3.5 trillion market cap. Its dominance reflects the ongoing AI boom and investor enthusiasm around high-performance computing. Currently, Nvidia’s chips are central to nearly all major AI innovations, giving it a crucial edge over competitors.

.

Sources:

All index and returns data from Norgate Data and Commodity Systems Incorporated and Wall Street Journal

W E Sherman & Co., LLC. W E Sherman & Co., LLC. News from Reuters, Barron’s, Wall St. Journal, Bloomberg.com, ft.com, guggenheimpartners.com, zerohedge.com, ritholtz.com, markit.com, financialpost.com, Eurostat, Statistics Canada, Yahoo! Finance, stocksandnews.com, marketwatch.com, visualcapitalist.com, wantchinatimes.com, BBC, 361capital.com, pensionpartners.com, cnbc.com, FactSet, Morningstar/Ibbotson Associates, Corporate Finance Institute. LSEG I/B/E/S, Factset Earnings Insigh

Commentary from T Rowe Price Global markets weekly update — https://www.troweprice.com/personal-investing/resources/insights/global-markets-weekly-update

This report is provided for informational purposes only. This report does not constitute an offer to sell or a solicitation or an offer to buy any securities. Any reference to a specific security included in this report does not constitute a recommendation to buy, sell or hold that security. Consult with your advisor for advice. All investments involve risk, including loss of principal. Principal values and investments returns are neither guaranteed nor issued by, guaranteed by, or obligations of a bank, savings and loan, or credit union; and are not insured or guaranteed by the FDIC, SIPC, NCUSIF or any other agency. Advisory Services offered through Harvest Investment Services, LLC, a Registered Investment Advisor.

Market Focus for the Week Ending on May 2nd, 2025

Market Focus for the Week Ending on May 2nd, 2025

Stocks down over tariff concerns:

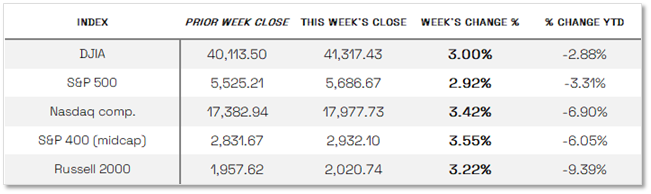

U.S. stocks ended the week on a high note, with the S&P 500 Index marking its second consecutive week of gains—the first such streak since January—and closing Friday with a nine-day winning streak. The Nasdaq Composite jumped 3.42%, buoyed by better-than-expected earnings from several large-cap tech companies, while small- and mid-cap indexes posted gains for the fourth straight week. Early optimism stemmed from easing trade tensions, as President Trump scaled back tariffs on cars and auto parts, and Commerce Secretary Howard Lutnick suggested a major trade agreement was nearing completion. As the week progressed, attention turned to earnings, with nearly 40% of the S&P 500’s market cap reporting first-quarter results, including four of the Magnificent Seven. Despite ongoing uncertainty around trade policy and limited forward guidance from companies, investor sentiment remained upbeat, with many confident that businesses could navigate slower economic growth and trade-related challenges

DOW & TECH

THE DOW JONES INDUSTRIAL AVERAGE (DJIA) is the oldest continuing U.S. market index with over 100 years of history and is made up of 30 highly reputable “blue-chip” U.S. stocks (e.g. Coca-Cola Co., Microsoft).

The Dow ended the week up 3.00% at 41,317.43.

THE NASDAQ COMPOSITE INDEX tracks most of the stocks listed on the Nasdaq Stock Market – the second-largest stock exchange in the world. Over half of all stocks on the NASDAQ are tech stocks.

The tech-driven Nasdaq ended the week up 3.42%, closing at 17,977.73.

LARGE, MEDIUM, & SMALL CAP

THE S&P 500 LARGE-CAP INDEX is a market-capitalization-weighted index of 500 leading publicly traded companies in the U.S. The S&P 500 is regarded as one of the best gauges of prominent American equities’ performance, and by extension, that of the stock market overall.

The S&P 500 ended the week up 2.92%, closing at 5,686.67.

THE S&P 400 MID-CAP INDEX is the benchmark index made up of 400 stocks that broadly represent companies with midrange market capitalization between $3.6 billion and $13.1 billion. It is used by investors as a gauge for market performance and directional trends in U.S. stocks.

The S&P 400 mid-cap ended the week up 3.55%, closing at 2,932.10.

THE RUSSELL 2000 (RUT) SMALL-CAP INDEX measures the performance of the 2,000 smaller companies included in the Russell 3000 Index. The Russell 2000 is managed by London’s FTSE Russell Group and is widely regarded as a leading indicator of the U.S. economy because of its focus on smaller companies that focus on the U.S. market.

The Russell 2000 ended the week up 3.22%, closing at 2020.74.

U.S. COMMODITIES / FUTURES OVERVIEW

THIS WEEK’S ECONOMIC NEWS

Mixed Economic Data:

This week’s economic data presented a mixed view of the U.S. economy, with job openings declining but hiring remaining resilient. The Bureau of Labor Statistics reported that job openings fell to 7.2 million in March—the lowest since September—indicating potential softening in labor demand amid economic uncertainty. ADP’s report showed private payrolls increased by just 62,000 in April, a sharp drop from March’s revised 147,000. However, Friday’s BLS payrolls report offered a more optimistic signal, with 177,000 jobs added in April—well above expectations—while the unemployment rate held steady at 4.2% and wages rose modestly. Stocks responded positively to the upbeat labor data. Meanwhile, the Bureau of Economic Analysis announced that GDP contracted at an annual rate of 0.3% in the first quarter, marking the first decline since 2022, driven by increased imports, slower consumer spending, and a drop in government outlays—likely influenced by companies accelerating purchases ahead of new tariffs. On a brighter note, the PCE Price Index was flat in March and consumer spending rose 0.7%, suggesting economic resilience and easing inflation pressures, though the full impact of recent tariffs has yet to be reflected.

Earnings Focus:

The 1st Quarter 2025 earnings reporting is ongoing, with 74% or 357 companies having reported earnings. Of the companies that have reported, 74% have reported earnings above analyst expectations. This is below the five and ten-year average of 77% and 75%. The projected Year over Year earnings growth rate for the S&P 500 is currently 13.6% while YOY revenue growth is 4.6%.

When you examine the individual sectors, seven of the eleven sectors are estimated to report a year-over-year increase in earnings. The Health Care and Communications sectors have the highest earnings growth rate for the quarter, while the Energy sector has the lowest anticipated growth compared to Q1 2024. The forward four-quarter P/E ratio of the S&P 500 is 20.6, which is above the ten and thirty-year average.

During the upcoming week, 92 S&P 500 companies (with 1 Dow 30 components) are scheduled to report results for the first quarter.

THIS WEEK’S HIGHLIGHTED STORY

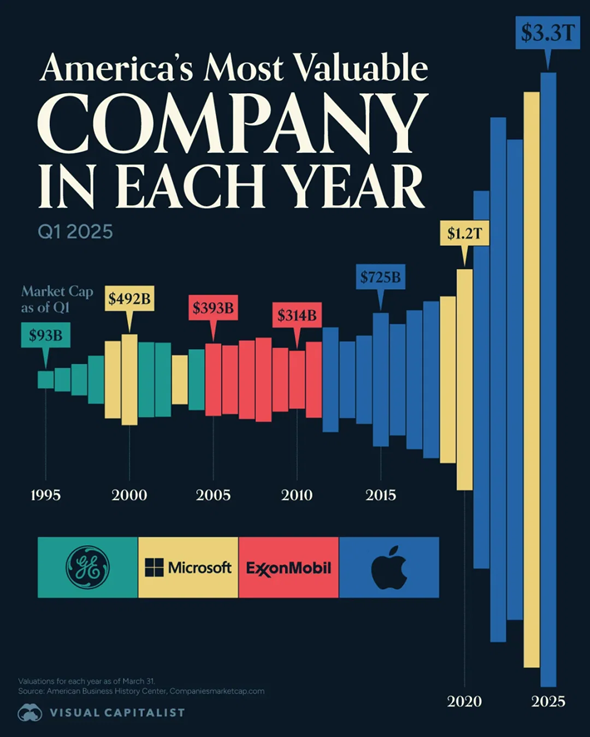

https://www.visualcapitalist.com/americas-most-valuable-company-in-each-year-1995-2025/

May 1, 2025

What We’re Showing:

While industrial giants like General Electric were once the most valuable companies by market capitalization, they’ve since been overtaken by tech-driven firms like Apple and Microsoft.

This transition reflects the economy’s pivot from manufacturing and energy toward software, data, and digital infrastructure. In recent years, investor enthusiasm for AI has driven valuations to historic highs, with trillion-dollar companies becoming a new normal.

In this graphic, we highlight America’s most valuable company in each year since 1995, based on Q1 market cap. Numbers are not adjusted for inflation.

Key Takeaways:

Apple and Microsoft Trade Places at the Top

Apple and Microsoft have dominated their competition for many years, frequently swapping places as the biggest company in the United States.

Apple’s ascent is fueled by its ecosystem of consumer electronics and services, particularly the iPhone. Microsoft, on the other hand, owes its valuation to its commanding share of the enterprise software (e.g. Office 365) and cloud computing sectors.

Both companies are developing artificial intelligence and have been working on integrating it into their respective offerings.

Nvidia’s Brief Moment at #1

Nvidia briefly disrupted Apple and Microsoft’s duopoly when it became America’s most valuable company on two occasions in 2024 (June and October).

The company’s massive boom is the result of its GPUs being critical for AI data-center expansion, and a belief that AI-driven technologies will rapidly reshape the world’s industries.

.

Sources:

All index and returns data from Norgate Data and Commodity Systems Incorporated and Wall Street Journal

W E Sherman & Co., LLC. W E Sherman & Co., LLC. News from Reuters, Barron’s, Wall St. Journal, Bloomberg.com, ft.com, guggenheimpartners.com, zerohedge.com, ritholtz.com, markit.com, financialpost.com, Eurostat, Statistics Canada, Yahoo! Finance, stocksandnews.com, marketwatch.com, visualcapitalist.com, wantchinatimes.com, BBC, 361capital.com, pensionpartners.com, cnbc.com, FactSet, Morningstar/Ibbotson Associates, Corporate Finance Institute. LSEG I/B/E/S, Factset Earnings Insight

Commentary from T Rowe Price Global markets weekly update — https://www.troweprice.com/personal-investing/resources/insights/global-markets-weekly-update

This report is provided for informational purposes only. This report does not constitute an offer to sell or a solicitation or an offer to buy any securities. Any reference to a specific security included in this report does not constitute a recommendation to buy, sell or hold that security. Consult with your advisor for advice. All investments involve risk, including loss of principal. Principal values and investments returns are neither guaranteed nor issued by, guaranteed by, or obligations of a bank, savings and loan, or credit union; and are not insured or guaranteed by the FDIC, SIPC, NCUSIF or any other agency. Advisory Services offered through Harvest Investment Services, LLC, a Registered Investment Advisor.

Market Focus for the Week Ending on June 6th 2025

Market Focus for the Week Ending on June 6th 2025

Stocks Continue Up Last Week:

U.S. stocks climbed for the second consecutive week, with small-cap stocks leading the gains as the Russell 2000 Index rose 3.19%, followed by the Nasdaq Composite up 2.18% and the Dow Jones Industrial Average up 1.17%, all joining the S&P 500 in positive territory for the year. Information technology stocks outperformed, buoyed by optimism around artificial intelligence (AI) following strong corporate earnings and news that Meta Platforms signed a 20-year deal with Constellation Energy to support its AI operations. Meanwhile, trade tensions between the U.S. and China resurfaced after social media comments from President Donald Trump, though a phone call between Trump and President Xi Jinping later in the week offered a more hopeful tone, with Trump describing the discussion as reaching “a very positive conclusion for both countries”

DOW & TECH

THE DOW JONES INDUSTRIAL AVERAGE (DJIA) is the oldest continuing U.S. market index with over 100 years of history and is made up of 30 highly reputable “blue-chip” U.S. stocks (e.g. Coca-Cola Co., Microsoft).

The Dow ended the week up 1.17% at 42,762.87.

THE NASDAQ COMPOSITE INDEX tracks most of the stocks listed on the Nasdaq Stock Market – the second-largest stock exchange in the world. Over half of all stocks on the NASDAQ are tech stocks.

The tech-driven Nasdaq ended the week up 2.18%, closing at 19,529.95.

LARGE, MEDIUM, & SMALL CAP

THE S&P 500 LARGE-CAP INDEX is a market-capitalization-weighted index of 500 leading publicly traded companies in the U.S. The S&P 500 is regarded as one of the best gauges of prominent American equities’ performance, and by extension, that of the stock market overall.

The S&P 500 ended the week up 1.5%, closing at 6,000.36.

THE S&P 400 MID-CAP INDEX is the benchmark index made up of 400 stocks that broadly represent companies with midrange market capitalization between $3.6 billion and $13.1 billion. It is used by investors as a gauge for market performance and directional trends in U.S. stocks.

The S&P 400 mid-cap ended the week up 1.66%.

THE RUSSELL 2000 (RUT) SMALL-CAP INDEX measures the performance of the 2,000 smaller companies included in the Russell 3000 Index. The Russell 2000 is managed by London’s FTSE Russell Group and is widely regarded as a leading indicator of the U.S. economy because of its focus on smaller companies that focus on the U.S. market.

The Russell 2000 ended the week up 3.19%.

U.S. COMMODITIES / FUTURES OVERVIEW

THIS WEEK’S ECONOMIC NEWS

Mixed Economic Data:

May’s economic data offered a mixed but slightly more positive picture of the U.S. economy, with job growth slowing yet outperforming expectations and other indicators showing signs of strain. The Labor Department reported 139,000 new nonfarm payrolls in May—down from April’s revised 147,000 but above the forecasted 130,000—while the unemployment rate held steady at 4.2%. The upbeat jobs report, which followed weaker data from ADP and rising initial jobless claims, helped lift both stocks and Treasury yields. Meanwhile, job openings and hiring picked up in April, suggesting continued labor demand despite the start of broad tariffs under the Trump administration. However, manufacturing activity shrank for the third straight month, with the ISM PMI dropping to 48.5%—its lowest level since November—while services activity also unexpectedly contracted for the first time in nearly a year, registering a PMI of 49.9%. Despite falling demand, prices remained high in both sectors, and while new orders dropped sharply, service sector employment rebounded into expansion territory.

Earnings Focus:

The 1st Quarter 2025 earnings reporting is ongoing, with 99% or 496 companies having reported earnings. Of the companies that have reported, 76% have reported earnings above analyst expectations. This is below the five and ten-year average of 77% and 75%. The projected Year over Year earnings growth rate for the S&P 500 is currently 13.7% while YOY revenue growth is 5.0%.

When you examine the individual sectors, nine of the eleven sectors are estimated to report a year-over-year increase in earnings. The Communications and Materials sectors have the highest earnings growth rate for the quarter, while the Real Estate sector has the lowest anticipated growth compared to Q1 2024. The forward four-quarter P/E ratio of the S&P 500 is 22.0, which is above the ten and thirty-year average.

During the upcoming week, 2 S&P 500 companies (with zero Dow 30 components) are scheduled to report results for the first quarter and two companies are scheduled to report for the second quarter.

THIS WEEK’S HIGHLIGHTED STORY

https://www.visualcapitalist.com/u-s-manufacturing-by-state-who-gains-most-from-made-in-america/

June 6, 2025

What We’re Showing:

President Trump has championed the idea that a key part of making America great again is bringing back industries that left the country in recent decades. With his tariff-driven trade policy, the White House has promoted “Made in America” as a way to create jobs and boost the economy.

Based on April 2025 data from the Bureau of Labor Statistics, this map highlights the U.S. states leading and lagging in manufacturing employment.

Key Takeaways:

Several Southern states have also built strong manufacturing bases. North Carolina (459,300), Georgia (426,500), and Tennessee (364,300) each rank among the top states, supported by industries such as automotive, aerospace, and food processing.

Wisconsin, ranked in the top 10 for total manufacturing employment, stands out for outperforming its size. Although it’s only the 20th most populous state, its manufacturing base remains strong, thanks in part to food and dairy processing. In per capita terms, it’s number one in the nation with 7,763.8 manufacturing jobs for every 100,000 people.

Florida, another top 10 state, has emerged as a growth story. Between 2019 and 2023, the state’s manufacturing employment grew by nearly 10%, highlighting the sector’s expansion in one of the country’s largest economies.

At the other end of the spectrum, Wyoming (10,600 jobs), Alaska (11,900), and Washington, D.C. (1,200) recorded the lowest levels of manufacturing employment. The latter (D.C.) also has the lowest numbers per capita.

Sources:

All index and returns data from Norgate Data and Commodity Systems Incorporated and Wall Street Journal

W E Sherman & Co., LLC. W E Sherman & Co., LLC. News from Reuters, Barron’s, Wall St. Journal, Bloomberg.com, ft.com, guggenheimpartners.com, zerohedge.com, ritholtz.com, markit.com, financialpost.com, Eurostat, Statistics Canada, Yahoo! Finance, stocksandnews.com, marketwatch.com, visualcapitalist.com, wantchinatimes.com, BBC, 361capital.com, pensionpartners.com, cnbc.com, FactSet, Morningstar/Ibbotson Associates, Corporate Finance Institute. LSEG I/B/E/S, Factset Earnings Insight

Commentary from T Rowe Price Global markets weekly update — https://www.troweprice.com/personal-investing/resources/insights/global-markets-weekly-update